IntervalTree.rs

Implemented an efficient interval tree in Rust and exposed PyO3 python bindings. GitHub repo.

Implemented an efficient interval tree in Rust and exposed PyO3 python bindings. GitHub repo.

The MCP server provides end-to-end workflows for SEC filings and earnings call transcripts—including ticker resolution, document retrieval, OCR, embedding, on-disk resource discovery, and semantic search—exposed via MCP and powered by the same olmOCR and embedding backends as vLLM backends. GitHub repo.

Completed the Tensor Puzzles, GPU Puzzles, and Helion and Triton Puzzles

This playlist is about going from theory to practice for training large models. Watch the playlist.

Parameter-efficient finetuning with ReFT (representation finetuning) on OLMoE-7B-A1B using interventions before and after MoE layers. GSM8k test loss: base 0.82, pre-MoE 0.91, post-MoE 10.8 (worse). GitHub repo.

Developed a weight-based aggregation of key-value heads to improve T5-small summarisation performance by 2.75% over the grouped query attention baseline. Explore the GitHub repo and the Weights & Biases report.

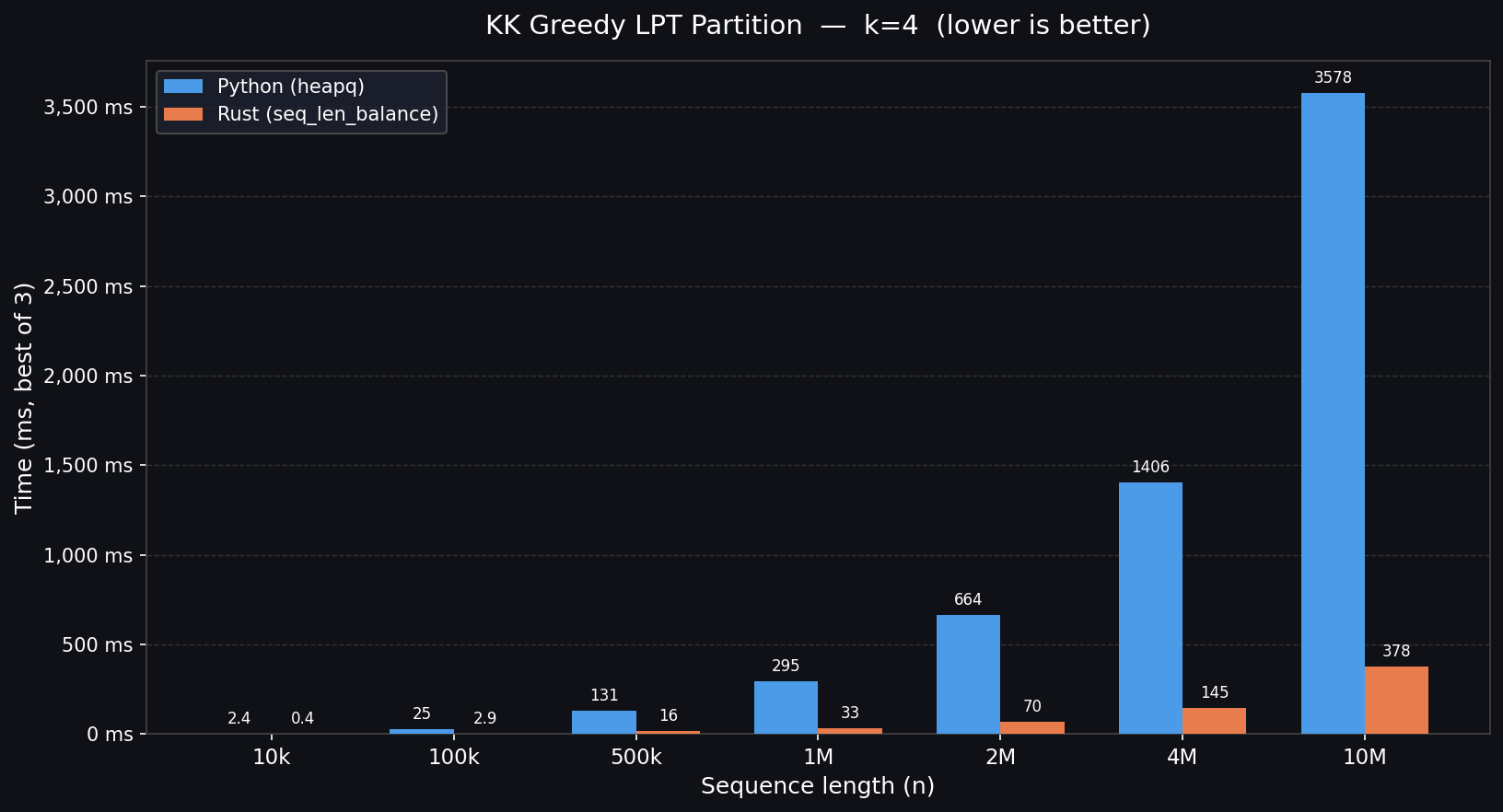

Built a Rust project for sequence length balancing with a scheduler backed by a ZMQ server using a ROUTER-DEALER architecture. See the GitHub repo.

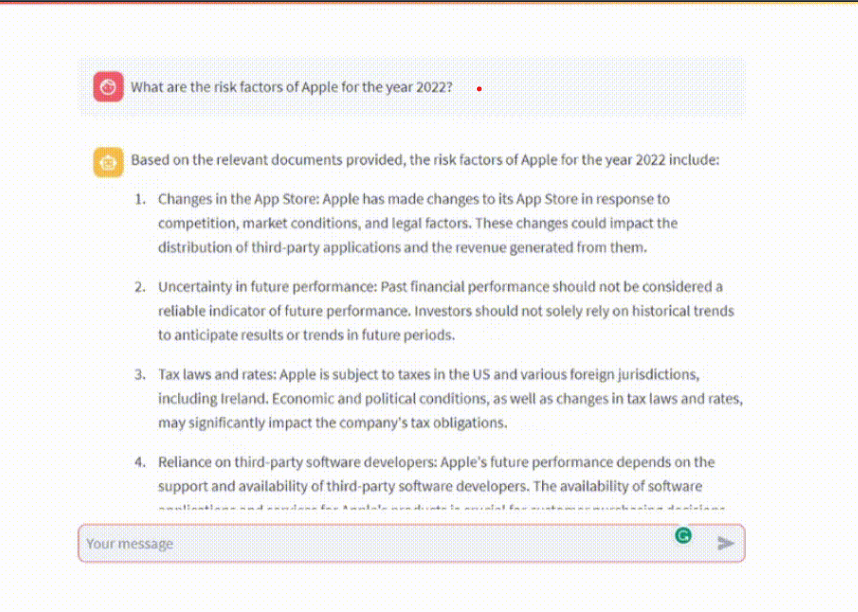

Built an end-to-end system that parses 10-Q and 10-K filings to answer investor

questions about company health. Explore the original

project and the revamped

finance data LLM repo.

Added specialised loaders to LlamaHub for SEC filings, IMDB reviews, and earnings call transcripts.

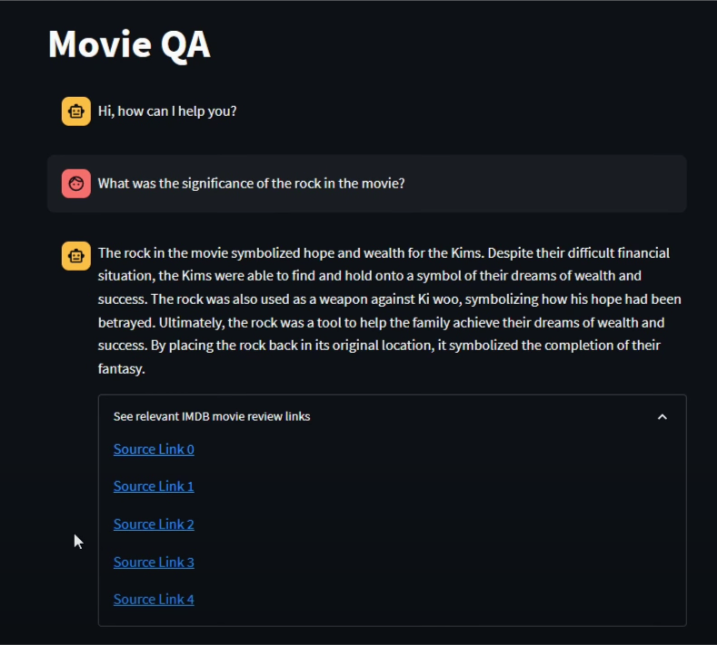

Built a MongoDB Atlas-powered QA system. Browse the code and watch the demo.

Leveraged web search data as state space to improve RL trading performance. GitHub · Medium

Work-in-progress on applying RL to portfolio construction. GitHub

Authored explainers and tutorials for hyperparameter optimisation workflows in FinRL. Article series

Selected projects that showcase classical ML techniques in finance settings.

Structured notes from the Coursera specialisation on investment management.

End-to-end financial modelling notebooks built during the specialisation.

Explorations of optimisation dynamics and convergence guarantees.

Assignments covering parsing, generation, and probabilistic modelling.

Topic modelling implementation tuned for finance corpora.

Bayesian regression templates for robust portfolio analytics.